Would Tiered Service Levels Be Fair or Cumbersome to Compute Cash-Out?

The State of Fintech and the Rise of Small Payment Cashing

As an observer of the nooks and crannies of the fintech world, it’s hard for me not to constantly be in awe of its very raw, very adaptive nature. It’s a maturing ecosystem that’s moving at the pace of necessity. Among the strongest of them is the small pay cashing service. In Korean, it’s something called 소액결제 현금화, or the act of converting the credit limit on your mobile phone plan into life money that you can spend on things that are not your mobile phone. It is a lifeline for many, a convenience for others, and a service that platforms like payiw have made it remarkably accessible.

For the most part, these services work on a simple, all-or-nothing basis. You want to cash out a sum, and there’s a fee. It’s simple, quick, and gets the job done for the immediate moment. But I’ve been struggling lately with the question that I think lies at the heart of the industry’s future. I have been wondering whether this simple model truly is the best one. What if we gave a little more? What if they introduced differentiated levels of service? My gut says that it’s a double-edged sword. Fair, on the one hand, to the gnarled depth. On the other, it could smother a beautifully simple process with the red tape of complexity.

My Vision for What a Tiered System Could Look Like

But before we go any further into the pros and cons, we should probably just imagine what a tiered small payment cashing system might look like. And that’s not just about charging different prices or not; it’s about designing a value ladder users can choose to ascend. If I had to design this model based on the patterns that I have observed across industries, I would probably create a tiered leveled model.

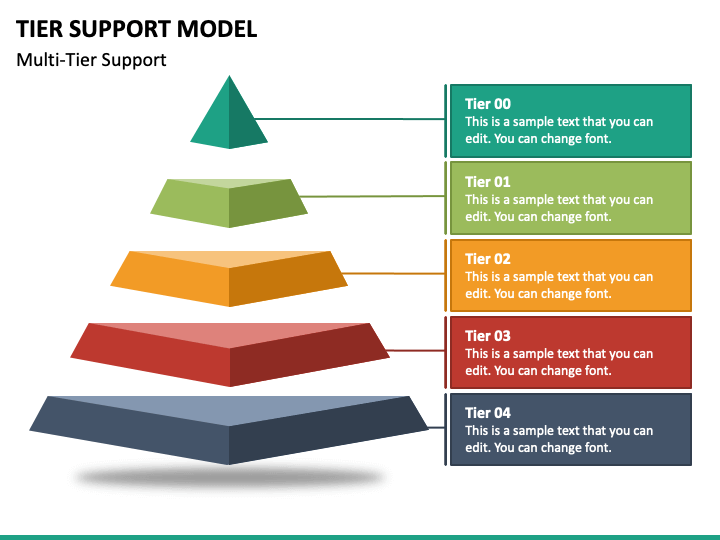

The Bronze Tier: The Gateway. That would be the standard level for any new unverified user. The process would still be the same as it is now fast and anonymous. The trade-off? They would charge the highest fees, and processing times could conceivably be a normal 12-24 hours. The cash-out maximum would be on the lower side. Who is the most likely to use this system? Single user and/or who can’t be bothered with a wait or wants maximum protection REGARDLESS of cost.

Tier 2: The Silver Level User – The Trusted Person. To at least be permitted to this level, a user might have to go through a straightforward, one-time verification for instance, verifying their identity or linking a bank account with a name and face matching theirs. They may also earn access simply after several successful transactions. The payoff for this tiny leap of confidence-building would be actionable: a significantly lower fee, quicker-clearing times (perhaps 1–3 hours) and a higher cash-out ceiling. In my opinion, this tier would become the “normal user” standard.

The Gold/VIP Tier: The Loyal Partner. This would be the elite category, for the very long-duration, very high-frequency users. A possible entry criteria might be their previous transaction history, for e.g., over a period of several months. For this loyalty, they would be offered the best possible terms: the lowest fees, instant or near-instant processing of cash-outs, the highest possible limits and perhaps even a dedicated customer-support channel. This tier turns the service from a mere transaction into a sustained financial relationship.

The above structure takes the service out of the asking 콘텐츠이용료 상품권 구매 and toward a more active conversation about the worth of trust and loyalty.

The Case for Fairness: Why I think Tiers could be a good thing

My bias for this way of doing things, the idea of fairness. In finance, fairness is not that you treat everyone the same; it’s that price should be linked to risk, and that good behavior should be rewarded. As I see it, a tiered approach does this in a few important ways.

Rewarding Proven Loyalty A one-size-fits-all fee structure lumps a brand-new user in with someone who has been responsibly using the service for a year. I find this fundamentally inequitable. This is a customer that you know is loyal. They have a track record. A ‘tiered system’ enables a platform to recognise and reward this loyalty with improved terms. This promotes a more healthy, sustainable relationship and provides incentive for good behaviour, in terms of both the user and the platform.

True Risk-Based Pricing In truth, there is a simple reason why the fees paid for mobile payment cash services can be relatively high. Much of that fee is meant to cover the cost of risk. You have the potential for fraud, chargebacks and managing stolen accounts. When I did some research into the kinds of fraud there are for these services, I realised that risk is really only associated with new or anonymous or illicit users.

Sure it does for a not start-uppy business with a proven track record that’s been your responsible and verified customer for a long time. Only then, by any financial measure, is it lower risk. Risk-based pricing, which underpins the way both the insurance and lending industries operate, says that lower risk should equal lower price. It’s the reason a safe driver pays less for car insurance. Using this logic, it should also be fair that a known, loyal party would have to pay less than an unknown party. A graduated system is the ideal way to enact this concept, ensuring more fairness and efficiency in rates.

User Choice: A layered model allows the user to choose. Instead of getting a take-it-or-leave-it, market-determined rate, they get an option. When they need to desperately rush and if they never have used the service before they can go for Bronze Tier and speed and anonymity. If they intend to take up the service more than once, they can be incentivized to take an action such as being verified which enables better terms. This kind of power over their financial terms is fair but something the current model does not allow for.

And now for the counterargument: The case for simplicity, or the many ways in which I believe tiers cause trouble

Now I need to put on my other hat: the user experience kind. No fax applications are a definite advantage to these small payment cashing services and the biggest of all is their amazing simplicity. They are an urgent solution, and urgency doesn’t have the patience for friction. This is the area where I think tiers have the power to hurt more than they help.

Enter the Friction and Decision Paralysis: Picture yourself in a stressful predicament. You have a pending bill to pay by tomorrow and your car needs an unexpected repair and you need money now. So when you attend a platform such as payiw. com, you need just one button that gets cash.” Get ready to choose between Bronze, Silver and Gold packages, each of which with its own charges, limits and checks. That introduces cognitive load and “decision paralysis” at the exact moment a user is least able to handle it. What’s elegant about the current system is that you have to give it very little thought.

The moral point: It is the issue of the “poverty premium” that is my greatest concern. While a tiered system, with graduated access for more loyal users, seems fairer, it may be perceived as deeply unfair to the most vulnerable among us. Who is going to opt for the highest priced Bronze Tier? First time users are the most desperate. They may not have the time to wait for verification or the digital literacy to do so. This results in the system effectively charging what has been called a “poverty premium” and the person in greatest need paying the highest price. This is a disturbing ethical trade-off that deeply concerns me.

Complex to operate:

It’s significantly more difficult to operate a system with tiers from a platform perspective. It needs a more advanced back-end to keep track of user status, apply different fee structures, and / or work a verification process. Customer service staff must be trained to answer questions of the various tier plans. Marketing really needs to make sure to explain the value proposition of each tier without muddling prospective buyers. This extra operational overhead is an expense that may ironically impact your users through higher base fees.

Learning From The Community: My Quest for Similarities

To wrap my head around this better, I sought parallels across other industries that have faced this same issue.

The most common example of loyalty tiers is in the airline industry. Their Bronze, Silver, and Gold frequent fly status programs are genius for retaining customers. It works because the rewards (upgrades, accessible lounges) are greatly valued and the customer base travels often enough to really notice it. That’s a strong argument for loyalty statuses in a tiered system.

I then cast my eyes towards the Software-as-a-Service (SaaS) world. Basic, Pro and Enterprise plans are the standard configuration companies offer. This is effective because all users have different needs fundamentally. A lone freelancer doesn’t require the same features as a 500-person corporation. There’s less of this parallel with cash-out services, since the fundamental human need that undergirds it the desire for cash is close to universal.

But I believe the most powerful parallel is the insurance industry. Risk-based pricing is literally their entire business model. They collect information on you to estimate your risk profile and charge you accordingly. Large large payment cashing tiers would basically be a simplified version of this. By giving up more information (verification, a history of reliability), you are showing that you are a “safer bet” and as such are rewarded with a better price. This is the comparison that allows me to believe that this model is in fact financially reasonable and logically fair.

My Verdict: A Slow Step Toward Complicated Fairness

After considering both sides of this question, I have a settled position. I agree that adding tiers would complicate the process, but I see this as a natural maturation of an industry. The familiar one-size-fits-all formula, while simple, is too crude an instrument. It does not know trust, honor loyalty, or price risk properly.

Here is my verdict: The future of small payment cashing should be in tiers. But it has to be handled very delicately. I am not advocating for a five-point system with a dozen variables that would be confusing. I think a two-tiered or three-tiered type of system is the right way. There is a big difference between being an unverified customer for the first time and being a verified customer a subsequent time and the terms of service should make a distinction.

This transformation reflects a departure from the transactional, anonymous and cerebrally focused toward a more adult, relationship-based experience. It’s a “complex fairness” more complex than the existing system, yes, but fairer in a way that counts. It recognizes that not all users are equal, and it makes a system in which trust is a currency of real value.

For platforms like payiw. com, this is the new frontier. The approach isn’t about cleaving to simplicity at any cost, but rather about introducing a new layer of sophistication with care and consideration. The aim is to make a system that remains fast and available to the individual in need while also being smart and reasonable enough to reward the loyal customers upon whom they will depend for such long-term success.

read more : Emma Myers: The Bright Star Who Won Hearts With Her Authenticity